IRDAI Reporting is a Board Level Risk

IRDAI Reporting is a Board Level Risk

IRDAI Reporting is a Board Level Risk

IRDAI and IIB Regulatory Compliance

George Koshy

Regulatory reporting deserves the same attention as your core policy administration or claims platforms.

In most Indian insurers, IRDAI reporting still runs on a patchwork of Excel files, email trails and late-night fire drills. Yet the consequences of missed or erroneous filings are no longer “just a compliance problem”. They are visible at the CEO, CFO, CCO, and board level. Let’s look at why regulatory reporting has quietly become a board‑level risk issue, and why it deserves the same attention as your core policy administration or claims platforms.

The compliance challenge that became a strategic risk

Established insurers are already monitoring IRDAI regulatory compliance at the CXO and board level. Any errors or delays in key returns have substantial consequences such as supervisory scrutiny, reputational damage, and, in the worst cases, restrictions on business activity. What was once treated as a back-office chore has become paramount for business continuity.

The regulatory calendar is demanding. Insurers juggle monthly, quarterly, half‑yearly and annual submissions across areas such as financials, investments, reinsurance, corporate governance, unclaimed amounts, and more. To top this, timely data submissions to the Insurance Information Bureau of India (IIB) for life, general and health insurers have become a standard expectation. The message is clear that regulators want more data, more often, and with fewer errors.

Looking ahead, the proposed move to Ind AS based financial reporting for insurers from 1 April 2026 is another step up in complexity. It will increase the inter‑linkages between finance, actuarial, risk and regulatory reporting, and intensify the scrutiny on reported numbers. In such an environment, weak reporting processes are not just operationally painful but also strategically dangerous.

Why the current operating model is fragile

Despite this raised bar, the operating model in many insurers has not changed much. IRDAI compliance reporting is typically a manual task in Excel, stitched together by a small group of specialists who know where all the files and macros live. The risks inherent in this approach are structural, not incidental.

First, there is the sheer volume and complexity of reports. Teams manage large and numerous templates, each with their own layouts, validations, and cross checks. Errors in Excel are easy to make and tough to catch, especially when multiple people are editing different versions in parallel. Something as basic as matching internal lines of business to IRDAI defined LOB categories can become a repetitive, manual and error‑prone exercise every cycle.

Second, regulatory change compounds the problem. Every time IRDAI tweaks a format, introduces a new disclosure, or tightens a timeline, existing Excel models need to be reworked. This rework typically happens under time pressure, often near filing deadlines, and can cascade into multiple dependent files. The result is predictable. Stress across finance, actuarial and compliance teams, late‑night reconciliations, and heightened exposure for the CEO, CFO and Legal/Compliance heads when something slips.

Third, control and visibility are limited. CXOs and Legal/Compliance often have only a high-level view of the reporting process. They see the final numbers but have limited ability to perform quick sanity checks or drill from a reported figure back to its data source. When a board member or regulator asks, “Where does this number come from?”, answering that question can take days of manual tracing through spreadsheets, emails and system extracts.

Finally, as IRDAI and IIB move towards more data driven supervision, compliance timelines and expectations are only going to tighten. New frameworks, such as the one for fraud monitoring, that rely on IIB’s aggregated data will depend on high frequency, high quality submissions from insurers. An Excel centric operating model is not designed for that level of resilience.

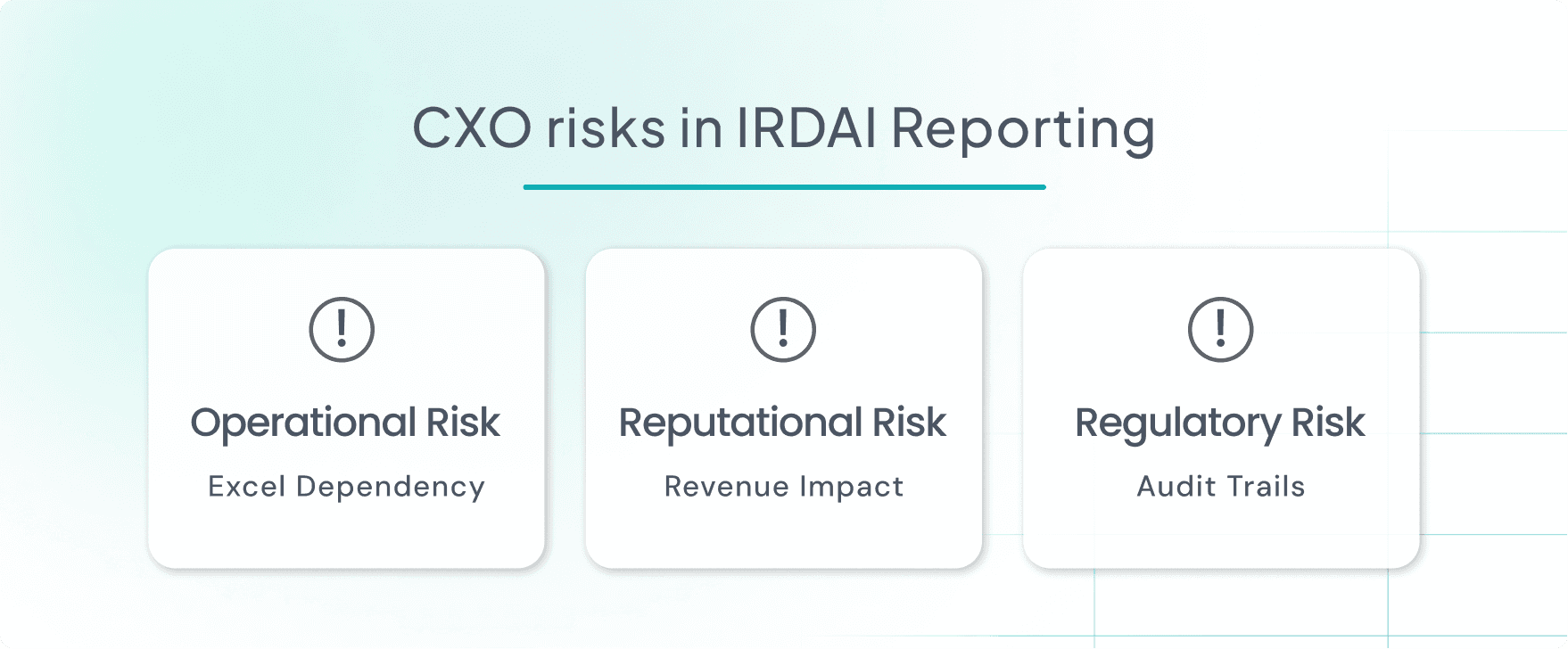

A CXO’s risk is operational, reputational and regulatory

From a CXO perspective, the current state creates three distinct risk layers.

Operational risk: Dependence on a handful of “Excel heroes” creates concentration risk. If one or two key people leave, are unavailable, or simply make a mistake under pressure, the entire reporting cycle can derail. There is little standardization in how templates are built and maintained, which makes onboarding new team members difficult.

Reputational risk: Inconsistent or late reporting erodes confidence with the regulator and can raise questions at the board level about management effectiveness. In an industry built on trust, repeated issues with basic compliance erode credibility with investors, partners, and even employees.

Regulatory risk: While many filings are viewed as routine, supervisors are increasingly using data for thematic reviews, peer comparisons, and early warning signals. Poor data quality or repeated corrections can trigger deeper scrutiny, onsite inspections, or directives to strengthen systems and controls.

These risks make IRDAI and IIB report a board level concern, not just a compliance checklist item. When regulatory reporting becomes a bottleneck, it affects product launches, portfolio shifts, and strategic initiatives that rely on clean, timely data.

Emerging platform mindset

Recognizing these risks, many insurers are beginning to treat regulatory reporting as a distinct layer in their architecture that is separate from, but tightly connected to, core systems. The aim is to move from a patchwork of spreadsheets to a platform driven model.

Platforms such as Kadac act as the “regulatory reporting engine” between internal systems and IRDAI. Seamless connection that standardizes data ingestion from source systems, Excel and data warehouses, configurable and governed master and mapping definitions to align internal LOBs and channels with IRDAI categorization and a library of pre-built templates aligned with IRDAI guidelines are offered within the platform apart from automated report generation and uploads, alerts for report deadlines, easier rework when LOB data changes and workflows with audit trails.

The result is not just efficiency, but resilience. Seamless, error free monthly, quarterly, half‑yearly and yearly IRDAI reporting, delivered on time at a lower cost, with a repeatable, trackable process that frees people for value added work. Instead of firefighting at month end, CXOs gain a controlled, transparent environment that can absorb regulatory changes and support the data driven supervision model that IRDAI and IIB are steadily building.

Regulatory reporting deserves the same attention as your core policy administration or claims platforms.

In most Indian insurers, IRDAI reporting still runs on a patchwork of Excel files, email trails and late-night fire drills. Yet the consequences of missed or erroneous filings are no longer “just a compliance problem”. They are visible at the CEO, CFO, CCO, and board level. Let’s look at why regulatory reporting has quietly become a board‑level risk issue, and why it deserves the same attention as your core policy administration or claims platforms.

The compliance challenge that became a strategic risk

Established insurers are already monitoring IRDAI regulatory compliance at the CXO and board level. Any errors or delays in key returns have substantial consequences such as supervisory scrutiny, reputational damage, and, in the worst cases, restrictions on business activity. What was once treated as a back-office chore has become paramount for business continuity.

The regulatory calendar is demanding. Insurers juggle monthly, quarterly, half‑yearly and annual submissions across areas such as financials, investments, reinsurance, corporate governance, unclaimed amounts, and more. To top this, timely data submissions to the Insurance Information Bureau of India (IIB) for life, general and health insurers have become a standard expectation. The message is clear that regulators want more data, more often, and with fewer errors.

Looking ahead, the proposed move to Ind AS based financial reporting for insurers from 1 April 2026 is another step up in complexity. It will increase the inter‑linkages between finance, actuarial, risk and regulatory reporting, and intensify the scrutiny on reported numbers. In such an environment, weak reporting processes are not just operationally painful but also strategically dangerous.

Why the current operating model is fragile

Despite this raised bar, the operating model in many insurers has not changed much. IRDAI compliance reporting is typically a manual task in Excel, stitched together by a small group of specialists who know where all the files and macros live. The risks inherent in this approach are structural, not incidental.

First, there is the sheer volume and complexity of reports. Teams manage large and numerous templates, each with their own layouts, validations, and cross checks. Errors in Excel are easy to make and tough to catch, especially when multiple people are editing different versions in parallel. Something as basic as matching internal lines of business to IRDAI defined LOB categories can become a repetitive, manual and error‑prone exercise every cycle.

Second, regulatory change compounds the problem. Every time IRDAI tweaks a format, introduces a new disclosure, or tightens a timeline, existing Excel models need to be reworked. This rework typically happens under time pressure, often near filing deadlines, and can cascade into multiple dependent files. The result is predictable. Stress across finance, actuarial and compliance teams, late‑night reconciliations, and heightened exposure for the CEO, CFO and Legal/Compliance heads when something slips.

Third, control and visibility are limited. CXOs and Legal/Compliance often have only a high-level view of the reporting process. They see the final numbers but have limited ability to perform quick sanity checks or drill from a reported figure back to its data source. When a board member or regulator asks, “Where does this number come from?”, answering that question can take days of manual tracing through spreadsheets, emails and system extracts.

Finally, as IRDAI and IIB move towards more data driven supervision, compliance timelines and expectations are only going to tighten. New frameworks, such as the one for fraud monitoring, that rely on IIB’s aggregated data will depend on high frequency, high quality submissions from insurers. An Excel centric operating model is not designed for that level of resilience.

A CXO’s risk is operational, reputational and regulatory

From a CXO perspective, the current state creates three distinct risk layers.

Operational risk: Dependence on a handful of “Excel heroes” creates concentration risk. If one or two key people leave, are unavailable, or simply make a mistake under pressure, the entire reporting cycle can derail. There is little standardization in how templates are built and maintained, which makes onboarding new team members difficult.

Reputational risk: Inconsistent or late reporting erodes confidence with the regulator and can raise questions at the board level about management effectiveness. In an industry built on trust, repeated issues with basic compliance erode credibility with investors, partners, and even employees.

Regulatory risk: While many filings are viewed as routine, supervisors are increasingly using data for thematic reviews, peer comparisons, and early warning signals. Poor data quality or repeated corrections can trigger deeper scrutiny, onsite inspections, or directives to strengthen systems and controls.

These risks make IRDAI and IIB report a board level concern, not just a compliance checklist item. When regulatory reporting becomes a bottleneck, it affects product launches, portfolio shifts, and strategic initiatives that rely on clean, timely data.

Emerging platform mindset

Recognizing these risks, many insurers are beginning to treat regulatory reporting as a distinct layer in their architecture that is separate from, but tightly connected to, core systems. The aim is to move from a patchwork of spreadsheets to a platform driven model.

Platforms such as Kadac act as the “regulatory reporting engine” between internal systems and IRDAI. Seamless connection that standardizes data ingestion from source systems, Excel and data warehouses, configurable and governed master and mapping definitions to align internal LOBs and channels with IRDAI categorization and a library of pre-built templates aligned with IRDAI guidelines are offered within the platform apart from automated report generation and uploads, alerts for report deadlines, easier rework when LOB data changes and workflows with audit trails.

The result is not just efficiency, but resilience. Seamless, error free monthly, quarterly, half‑yearly and yearly IRDAI reporting, delivered on time at a lower cost, with a repeatable, trackable process that frees people for value added work. Instead of firefighting at month end, CXOs gain a controlled, transparent environment that can absorb regulatory changes and support the data driven supervision model that IRDAI and IIB are steadily building.